DiNapoli: Tax Cap Set at 2% in 2023

Highest Inflation Since Start of Local Tax Cap Will Impact Local Governments

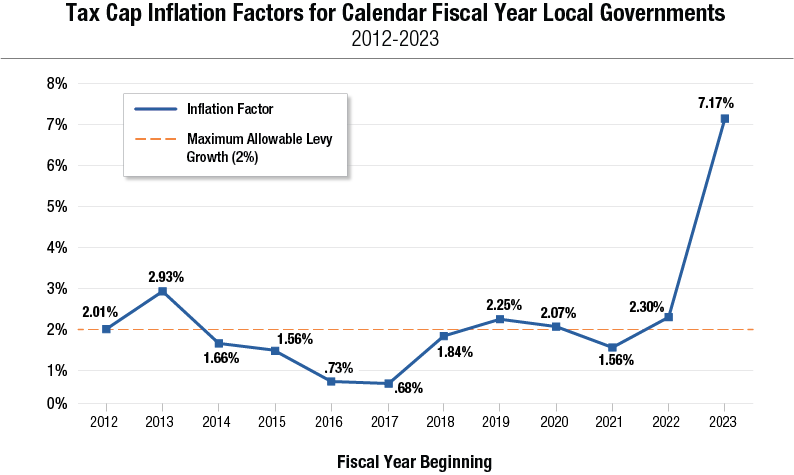

Property tax levy growth will again be capped at 2% for 2023 for local governments that operate on a calendar-based fiscal year, according to data released today by State Comptroller Thomas P. DiNapoli. This figure affects tax cap calculations for all counties, towns, and fire districts, as well as 44 cities and 13 villages.

“Allowable tax levy growth will be limited to two percent for a second consecutive year,” DiNapoli said. “Just as local governments are receiving their final round of federal funding under the American Rescue Plan Act, they are facing economic challenges that will likely drive costs higher than expected or planned, making it harder to adhere to the tax cap as they prepare their budgets for 2023.”

DiNapoli said given this year’s inflation factor calculation of 7.17%, a majority of New York’s counties, towns and calendar year cities and villages could see cost increases that exceed the amounts they are set to receive in their final round of American Rescue Plan Act (ARPA) funds.

The tax cap, which first applied to local governments and school districts in 2012, limits annual tax levy increases to the lesser of the rate of inflation or 2% with certain exceptions. The tax cap also includes a provision that allows municipalities to override the tax cap.

The 2% cap for the 2023 fiscal year is the fourth time since 2019 that municipalities with a calendar-based fiscal year (Jan. 1 through Dec. 31) had their levy growth capped at that amount. In accordance with state law, DiNapoli’s office calculated the inflation factor at 7.17% for those with a calendar fiscal year in 2023. This is the highest the inflation factor has been since the tax cap was first implemented and more than triple the 2.3% inflation factor from the prior year.

Chart

Allowable Tax Levy Growth Factors for Local Governments

Posted: July 13th, 2022 under Peru/Regional History, State Government News.